Getty Images; realtor.com

We know what some of you are thinking: Who’s thinking of buying a house right now? Well, in fact, plenty of people—even in the face of the mounting coronavirus pandemic and fears of a looming recession. Because life goes on. Mortgage rates are at all-time lows. And people need to buy homes for the same reasons they usually do—getting married, having kids, downsizing, retiring, or relocating.

But buying a home remains an incredibly intimidating task—and the first step, getting a mortgage, sometimes seems like facing a sheer cliff without climbing gear. You’ve got to make sure your credit is acceptable. You’ve got to look at your debt-to-income ratio and make sure your employment situation meets the standards of the bank.

And then there’s the biggest challenge of all: scraping together the cash for a 20% down payment.

That’s the amount typically recommended, since it means the lender won’t require you to tack on an extra monthly fee for private mortgage insurance. But apparently most people don’t put down 20% after all—the average down payment in January was just 11.4%, according to real estate data firm Optimal Blue. With mortgage rates so low, it’s not necessarily worth your while to sink all your cash into a down payment.

“It’s always good to put less down, so you’re not forcing yourself to spend all your money on the house,” says Donald Frommeyer, mortgage loan officer at CIBM Mortgage. “Everyone knows that when you walk into a house, you’re going to want to paint, replace the cabinets, or whatever. A small down payment gives the customer more money to do more with the house.”

As it turns out, down payments vary dramatically based on where in the U.S. you are looking to put down roots. So we zeroed in on the places in the U.S. where savvy home buyers are putting down the lowest percentage down—and the highest.

Most of these places on the lower end of the scale have plenty of homes that are affordable for first-time buyers and aren’t seeing crazy bidding wars. And more people there are taking advantage of low- or no-down payment loans from the Federal Housing Administration, the Department of Veterans Affairs (for active military members and veterans), or the Department of Agriculture (for low- to moderate-income buyers in less populated locations). Some of these cities even offer down payment assistance grants to help first-timers get into a home.

The other end of the spectrum? They tend to be notoriously high-priced metros like Los Angeles, New York City, and San Francisco, which basically require buyers to take out harder-to-obtain jumbo loans to get a toehold in the real estate market. While the threshold differs from county to county, many mortgages in such places are too big to be sold under Fannie Mae and Freddie Mac. They start at $484,350 and require a minimum of 20% down.

To figure out where down payments are the lowest and highest, the realtor.com® data team combed through stats from Optimal Blue to see how much cash buyers were putting down as a percentage of their home’s value. We looked at all purchase mortgages for all types of housing in the 100 largest U.S. metropolitan areas as of February 2020. The final list includes no more than two metros from any one state—otherwise the ranking for highest down payment would have been dominated by California cities.

Got it? Let’s start out by looking at where you might be able to get in on a home without selling a kidney.

Tony Frenzel

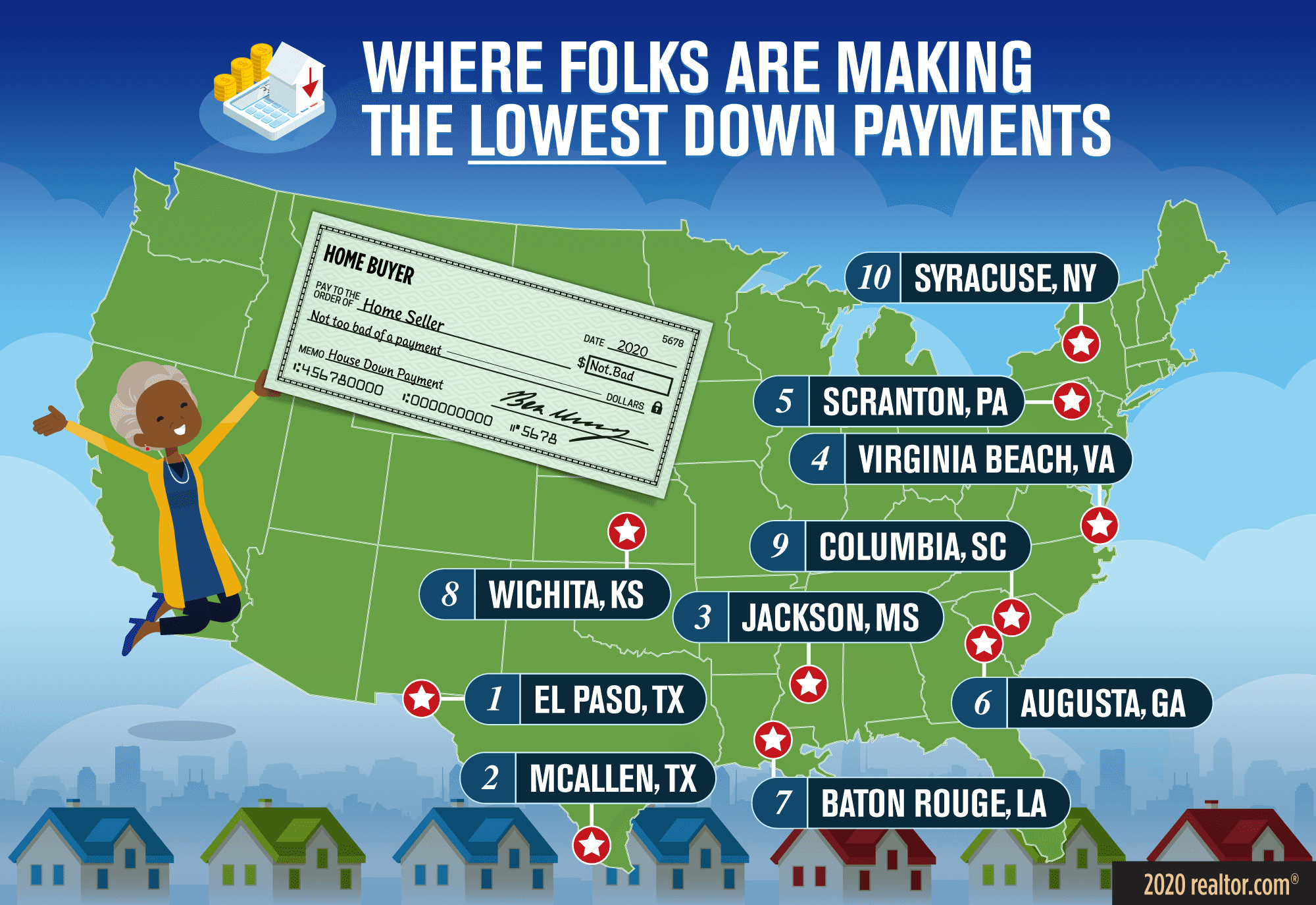

1. El Paso, TX

Average down payment: 4.97%

Median list price: $180,000

realtor.com

Emotionally, El Paso had a rough year in 2019. The city was rattled by a mass shooting in August, and residents are still overcoming the shock.

Economically, however, the Borderland city has been thriving. And home values have been steadily increasing, up 11% over last year, according to recent realtor.com data. And it’s (relatively) easy to get into a house even if you don’t have piles of cash sitting around. The median list price is nearly half the national number ($300,000), and there are many home builders offering low down payment incentives and military folks with VA loans.

In the desirable neighborhood of Castner Heights, buyers can get four-bedroom homes in a variety of styles—from Colonials to ranches—for $175,000 (or less). Or you can land a brand-new, four-bedroom home for just $192,950.

“Builders are paying closing costs and throwing incentives at buyers,” says Alex Cordova, a real estate agent with Alexander Cordova Luxury Real Estate. “You get a lot for your money here.”

2. McAllen, TX

Average down payment: 5.66%

Median list price: $209,000

realtor.com

An hour’s drive from the beautiful beaches of South Padre Island and just 5 miles from the Mexico border, McAllen is an affordable, family-friendly city that’s growing rapidly. Over the past decade, the population has increased 9%, with a whopping 30% of the city’s residents being under the age of 18.

Many of those growing young families have been moving to the economically stable metro from higher-priced areas in California and the Midwest to get a foothold in the city’s relatively easy-to-enter real estate market.

The median list price in McAllen, the center of the metro area, is just $209,000, well below the national $310,000. So, it’s attracting lots of first-time buyers who take advantage of 3.5% FHA and 3% conventional loans for inexpensive homes like this three-bedroom for $135,000 and this remodeled four-bedroom for $189,000.

“If I have 20 loans in a week, 18 will be first-time home buyers,” says Mariana Ortega, loan originator for Cabrales Mortgage, explaining why the average down payment is so low.

3. Jackson, MS

Average down payment: 5.76%

Median list price: $127,900

In 2019, USDA Rural Development set aside $18.5 million in zero-down loans to very low- and low-income rural Mississippi households, along with $415 million for moderate-income households. Because Jackson is relatively compact, locals don’t have to go too far from the city center to take advantage of those programs—and some of the most coveted neighborhoods are in those rural zones.

While the population in Jackson has decreased 5.3% over the past decade, family-friendly Flowood has surged 17.6%. That’s probably because it’s less than a 20-minute drive from all the jobs at the state Capitol and University of Mississippi, and 30 minutes from Nissan North America’s headquarters. Families can snap up nice homes in good school districts in Flowood, including this traditional three-bedroom listed for $199,750 and this $229,900 three-bedroom in sought-after Laurelwood, without putting down a penny.

4. Virginia Beach, VA

Average down payment: 6.5%

Median list price: $235,050

realtor.com

Eastern Virginia’s economy was healthy through 2019 and is expected to continue growing this year, despite the COVID-19-related hit to the local hospitality industry. That projected growth is due to increases in military spending. The area is home to the world’s largest naval base, Naval Station Norfolk, which means there are a whole lot of sailors, medical personnel, and other current and former members of the military who take advantage of zero-down VA loans. That helps to keep the percentage down on homes low throughout the metro.

The area boasts million-dollar-plus homes on the beach, but buyers can also find more affordable, single-family homes just a short drive away. They include this four-bedroom ranch, less than 10 minutes away from the sand, for $239,900 and even this brand-new, three-bedroom for $200,000 in South Norfolk, a six-minute commute from Norfolk Naval Shipyard.

5. Scranton, PA

Average down payment: 6.78%

Median list price: $108,000

After decades of economic bad luck—including closed coal mines and industrial plants—and a near miss with bankruptcy in 2012, the Scranton metro area has seen an uptick in real estate demand over the past couple of years. That’s mostly because it’s so cheap. Hordes of millennials who can’t afford to buy in places like New York City have been decamping for the home of their beloved show “The Office.” Those young(ish) buyers account for more than 50% of the mortgages in the metro, many of which are low down payment FHA loans.

Right in its revitalized downtown, urbanites can get into the Scranton market for a fraction of what they’d need in other major metros. Options include this sleek two-bedroom loft for just $203,000 or this two-bedroom condo within walking distance to the universities, restaurants, and everything else for—get this—just $79,999.

Rounding out the list of the places where buyers are putting the lowest percentage down are Augusta, GA (6.92%); Baton Rouge, LA (6.99%); Wichita, KS (7%); Columbia, SC (7.12%); and Syracuse, NY (7%).

———

Ready to jump to the other end of the mortgage spectrum? Let’s take a look at the places where buyers are coughing up the biggest chunk of their purchase price upfront.

Tony Frenzel

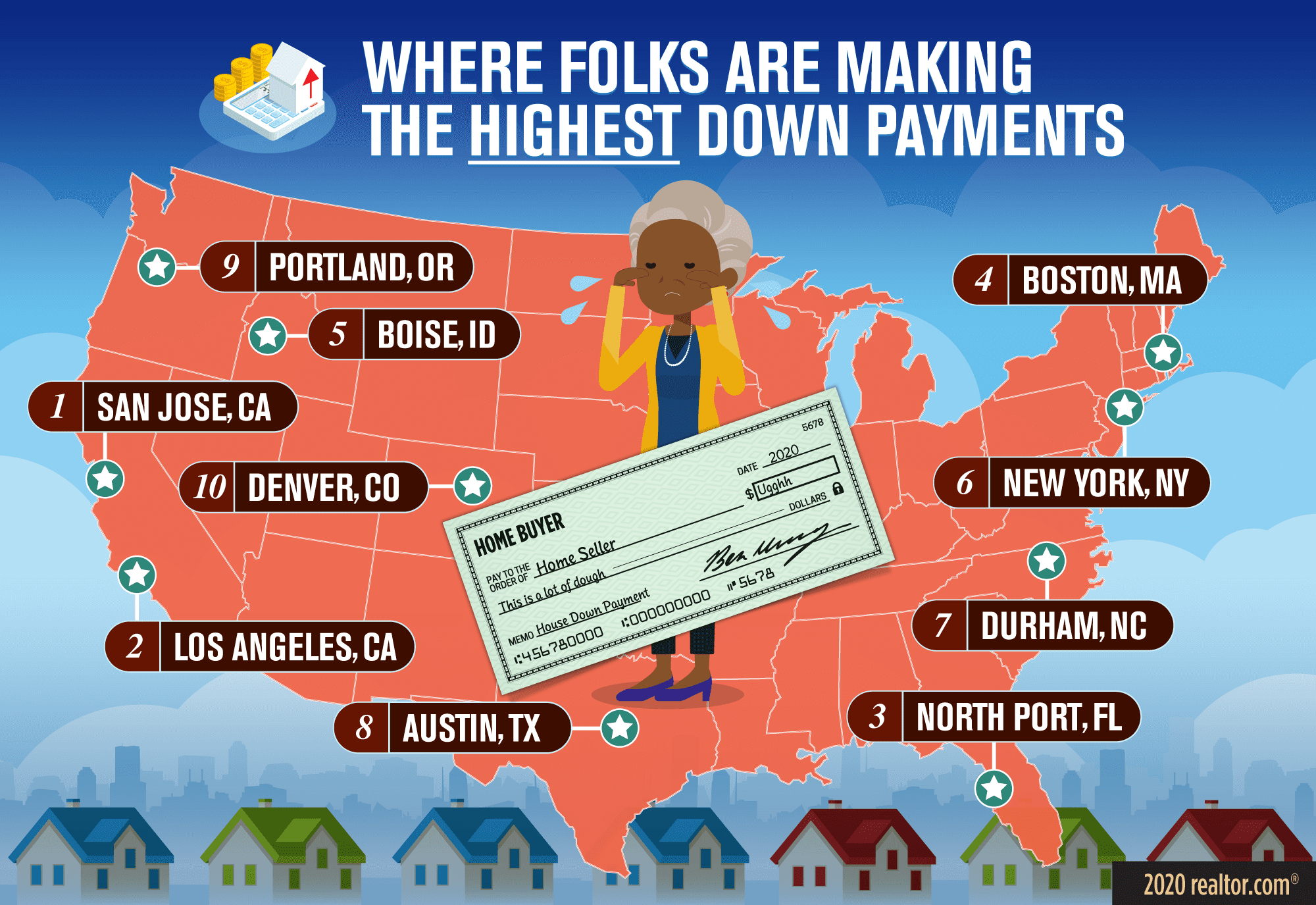

1. San Jose, CA

Average down payment: 20.84%

Median list price: $950,000

realtor.com

Silicon Valley is known for its well-paying tech jobs and equally high-priced homes, which means that most buyers who want to get into the market need to obtain a jumbo loan. The median list price in San Jose is $950,000, more than $200,000 above the high balance loan limit, which starts at $726,525.

The metro boasts condos and townhomes below the jumbo loan limit, according to mortgage broker loan agent Stephen Wong of Bayonne Real Estate, which buyers can get into for as little as 5% down. But as is the case throughout California, many locals prefer to have their own slice of land—which is convenient as everyone who can work remotely these days is doing so.

Entry-level, single-family homes—including this 1,134-square-foot, three-bedroom listed at $769,888 and this slightly larger four-bedroom for $899,000—require at least 20%.

“The price is high, so it basically requires a high down payment,” says Wong.

2. Los Angeles, CA

Average down payment: 19.61%

Median list price: $999,000

When interest rates dropped in mid-2019, Los Angeles’ already pricey real estate market was stoked even higher by buyers scrambling to get into homes. The all-cash offers that frustrated many a buyer without the means to fork over seven figures sans mortgage throughout 2017 were back.

The highly desirable single-family homes, the sleek midcentury modern units, and the Spanish-style bungalows in hot neighborhoods like Silver Lake (where the median list price is $1.3 million) and neighboring Los Feliz (a staggering $1.8 million) almost always require more stringent jumbo loans—starting at $726,525 in Los Angeles County—with a minimum of 20% down. And because the competition is so tight, sellers for places like this $1,375,000, two-bedroom in the hills and this sleek two-bedroom for $1,374,000 can pick and choose among buyers with more attractive loans and larger, easier-to-approve down payments.

“The average buyer out there is looking for that cute resale home with character,” says Mark Mullin, an agent with Tracy Do Compass. “Those homes, when in good condition, are the hardest to get, and people are willing to pay pretty high prices.”

3. North Port, FL

Average down payment: 16.56%

Median list price: $229,000

realtor.com

This will surprise no one: A lot of folks move to Florida to retire—especially at its tranquil Gulf Coast. According to Census Reporter, the median age in the North Port-Sarasota-Bradenton metropolitan statistical area is 53, 15 years older than the national median age of 38.

Of course retirees tend to have equity, which makes it a whole lot easier to throw down a nice chunk of change for the forever home of one’s dreams. Active folks who want plenty to do can buy into active 55-plus communities like this $174,900 two-bedroom in Lazy River Village in North Port or this $173,500 two-bedroom condo in Sarasota’s Strathmore Riverside Villas, one of the highest waterfront communities on the west coast of Florida.

“Retirees have lower income streams than they did when they worked, so the lenders may require larger down payments to compensate,” notes Brad O’Connor, chief economist for Florida Realtors®.

4. Boston, MA

Average down payment: 16.01%

Median list price: $775,000

Boston’s housing market has been on fire for the past several years. The median sales price has risen nearly $100,000 in the past two years alone. Skyrocketing home prices and tight competition in the seller’s market make scoring an abode in Boston hard enough, as sellers are able to pick and choose among buyers who present the most desirable loan packages or are willing to throw down buckets of cash. But adding insult to injury is the proliferation of condos and co-ops that are not FHA- or VA-approved.

“A lot of times in this city, loans with a low down payment don’t work,” says Jordan Bray, sales manager with Century 21 Cityside. “It’s not even an option for a lot of buildings.”

5. Boise, ID

Median down payment: 15.76%

Median list price: $370,300

realtor.com

Boise has been growing like gangbusters over the past several years. The metro’s population has skyrocketed 9.3% since 2010, and in 2018 it was ranked by Forbes as the fastest-growing city in the United States.

Microbreweries, trendy restaurants, and hip coffee shops are cropping up almost as quickly as luxury condos—and the city is now home to a booming tech scene fueled, in part, by Silicon Valley companies setting up shop to escape the sky-high costs of Northern California.

That inward migration from pricier locales is pushing up home costs, meaning the locals looking to sell have built up quite a bit of equity and the newcomers are often able to get a lot more bang for their buck and a lot lower mortgage payment every month. It’s why a recent Coldwell Banker report named Boise the nation’s top luxury market to watch.

“We’re still cheaper than much of the country,” says Rob Inman, director of operations at Boise’s Best Real Estate. “A lot of these buyers have a lot more equity when they move here and have more cash to put down.”

For less than the $600,000 it takes to get a one-bedroom condo in San Francisco, buyers in Boise can lay down roots in a gorgeous $559,000 four-bedroom in coveted Harris Mills Ranch District in Southeast Boise.

Filling out the 10 metros with the highest median down payments are New York City (15%); Durham, NC (14.88%); Austin, TX (14.33%); Portland, OR (14.2%); and Denver (13.97%).

The post Where Buyers Are Making the Lowest—and the Highest—Down Payments appeared first on Real Estate News & Insights | realtor.com®.

source https://www.realtor.com/news/trends/lowest-down-payment-cities/

No comments:

Post a Comment